Not only is embedded insurance changing the insurance industry, but it also impacts how individuals and companies see risk. These benefits are available to consumers and businesses that provide these perfectly integrated insurance products.

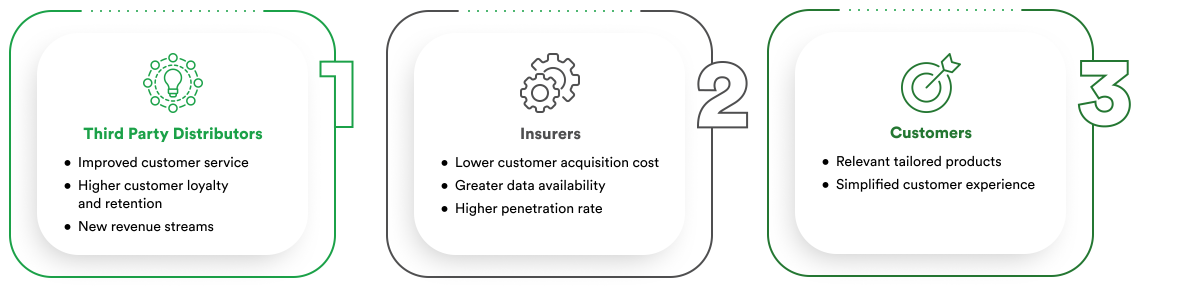

Benefits for customers

Convenience of Instant Coverage. The ease with which embedded insurance provides clients with coverage is one of its main benefits. Policyholders can easily access coverage at the time of need rather than through complicated insurance procedures. Embedded insurance guarantees quick and straightforward access to protection, whether to secure a gig work assignment, cover a trip, or insuring a new purchase.

Personalized Insurance Options. Embedded insurance meets the requirements of each client. Customers can tailor their coverage to meet particular needs. With this degree of personalization, policyholders can only pay for the required insurance, disregarding the need for universal plans and potential over insurance.

Potential Cost Savings. Consumers frequently experience cost savings from customized insurance policies. Customers can cut costs by purchasing insurance that properly fits their risk profile. Some embedded insurance services might also be more reasonably priced because of partnerships and reduced procedures.

Enhanced User Experience. Embedded insurance helps make users’ experiences better. Difficulty in purchasing is decreased by smoothly integrating insurance into current transactions or activities. Customers are happier because they are no longer required to leave a platform or fill out lengthy papers to obtain coverage.

A sense of trust. Embedded insurance gives customers trust. Knowing that insurance is in place provides security and assurance, whether protecting a pricey purchase, guaranteeing medical coverage when traveling, or defending against unforeseen mishaps in the gig economy.

Benefits for Businesses

Additional Revenue Streams. Embedded insurance offers organizations the chance to diversify their sources of income. Companies can increase revenue while fostering client loyalty by including insurance as a component of their goods or services.

Enhanced user experience. A seamless and user-friendly insurance experience can significantly improve the overall user experience of a business. Increased client retention, favorable ratings, and word-of-mouth recommendations may result.

Reduced Difficulty in the Purchase Process. Embedded insurance makes it less complicated for customers to complete transactions by reducing the friction in the purchase process. Higher conversion rates may arise from this, particularly for companies operating in marketplaces with intense competition.

Data-Driven Insights. Companies can use data from embedded insurance transactions to learn more about the preferences and behavior of their customers. Initiatives for customer interaction, product development, and marketing can all benefit from this data.

Risk management. Businesses can use embedded insurance to help control their goods or services risks. For instance, an electronic equipment manufacturer may provide product insurance to lessen the financial burden of warranty claims or returns.

Competitive Advantage. Businesses that provide embedded insurance may have an advantage over market rivals. The ease of insurance bundles can be a strong selling feature that draws in and keeps clients.

Opportunities for Partnership. To offer embedded insurance solutions, businesses might consider forming partnerships with insurers and InsurTech companies. These collaborations may provide access to cutting-edge knowledge and resources that improve the entire value proposition.